The purpose of this article is determine the fair release pricing for Bordeaux 2024 and compare it with the prices actually paid during the period. en primeur This campaign has now ended. The aim is twofold: to assess the consistency of châteaux’ pricing strategies with the market, and to provide a decision-making tool for industry players.

The rise and Fall of Bordeaux En Primeur

En primeur It has always been a rare opportunity for wine lovers: young wines are available at prices lower than vintages that have already been released.

But at the turn of the millennium, châteaux began to realize that they were leaving too much of the profit to the buyers. The case of Château Haut-Brion, which was the first of the 1st growths to release its 2005, and which gave up millions of euros in profit by setting the price too low, left its mark. The massive influx in speculators following the financial crisis only reinforced this feeling. Why build a great reputation and make great wine if a large part of it is lost to the estates at the end?

Bordeaux experienced a golden era in spring 2010, when the 2009 vintage was released. Prices soared. The frenzy waned in 2011. Bordeaux’s appeal was reduced by new markets, led primarily by China. Many speculators abandoned the market. But châteaux only partially adapted their prices. The prices of the 2011, 2012, 2013, and 2014 vintages are lower than those of their predecessors. They were less good in general than the 2009 and 2010 vintages.

The pandemic and the 2018-2020 trilogies briefly reignited interest. The momentum was never able to reach the heights seen in 2005 and 2009. The prices remained too high to encourage collectors or justify investments. Why purchase a wine that is still in barrels when you can buy a comparable vintage ready to drink at the same price.

The State of the Market by 2025

Prices of 2021,2022 and 2023 failed to revive demand. The 2021 vintage arguably stands out as one of the most striking examples of Bordeaux’s pricing misjudgment — a merely average year released at a price largely out of step with market reality. The exceptional 2022 vintage offered a chance to realign the pricing but was released at an excessively high level. Some châteaux, eager to enhance their image, pursued overly ambitious pricing strategies. This is a misinterpretation about the economics behind reputation and pricing. Reputation is not created by setting high prices. It is earned gradually, acknowledged by the market with prices increasing as a result. Bordeaux’s 2023 vintage was a final chance to reconnect with its markets. The 2023 vintage was excellent but not exceptional. It was positioned just behind the 2022 vintage, which is an interesting position. It could have been sold at the right price without (too much affecting) the recent great vintages. It is true that 2021 suffered. However, in any event, a wine sold at a high price will suffer a correction.

Bordeaux 2023s have been overpriced in reality and are hard to find. The value of 2021s has continued to drop since bottling. Even among the excellent vintages of 2018, 2019, and2020, there is little activity on the secondary market. Average listed prices do not reflect the actual levels of transactions, which are usually at least 10% less. Buyers adopt a wait-and see attitude, and only act if the price is truly compelling.

How to Calculate a Fair En Primeur Release Price

The method used is based around a simple economic principle. The latest vintage’s price must be comparable to vintages currently available on the marketplace. We estimate the effect of age, reputation and quality using data from 116 Crus (vintages between 2008 and 2023). We can then calculate for each wine the price at which a buyer is indifferent to a 2024 vintage or a previous vintage that has similar attributes (Masset, et. al., 2023). This exercise has been done for vintages 2021, 2022 You can also find out more about the following: 2023.

In recent years, this logic of arbitrage was not respected. Release prices for the 2024 vintage must fully align with these fundamentals of the market. Given the current weak demand, it is likely that prices will have to be set just below the estimated fair price to generate interest.

What Are the Release Prices for 2024?

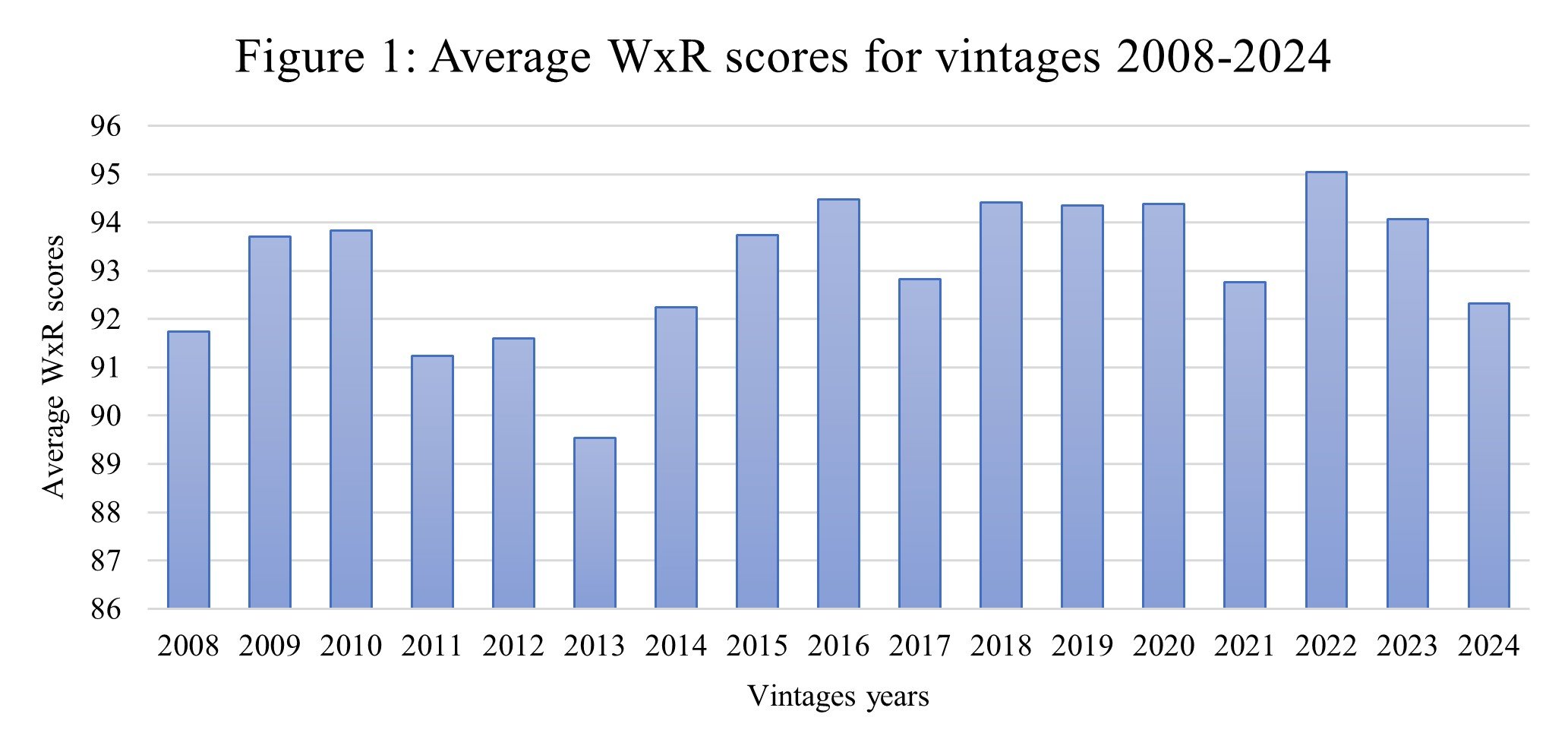

Compare the quality of 2024 and previous vintages. Wine Services has developed Wine Expert Ratings. These ratings are derived by standardizing and aggregating the scores of a representative panel of experts, providing one of the most accurate and objective measures of wine quality available (Cardebat & Paroissien, 2015). Figure 1 plots average WxR ratings for vintages 2008-2024. The 2024 harvest scores are lower than those of the great recent vintages. However, they are comparable to 2014, 2017 and 2020 and clearly better than 2013. This means that it’s not likely the weak vintage many had predicted at harvest. The vintage is good overall. It’s marked by low alcohol levels, and there is some heterogeneity.

— Source: EHL

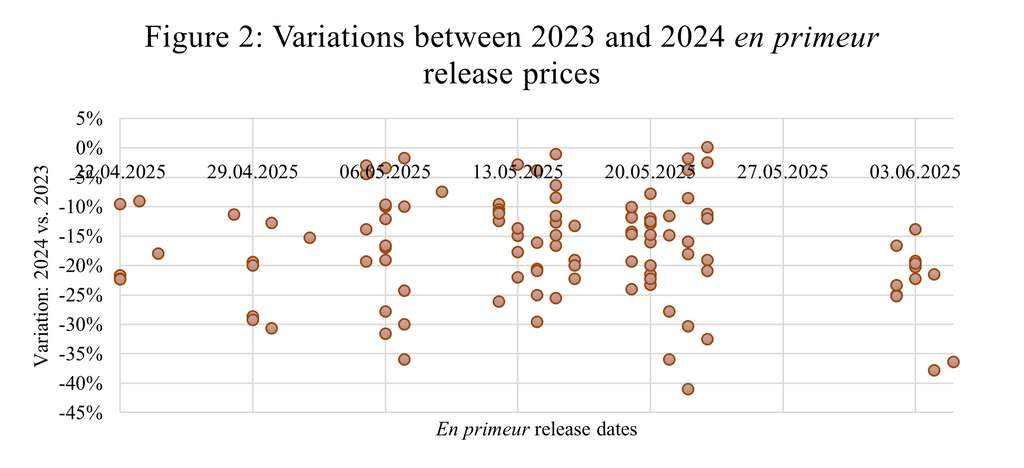

Figure 2 below shows the variations between this year’s and last year’s en primeur release prices for the same châteaux, with the release dates perhaps being part of a marketing strategy. First observation: prices have fallen sharply, by an average of 16%. Significant fluctuations can also be observed, with some wines remaining (more or less) stable, while others have lowered their prices by 30% to 40%. We can also see that there were significant drops already at the start of the en primeur campaign, but the biggest corrections relative to 2023 occurred at a time when the campaign was already well underway.

— Source: EHL

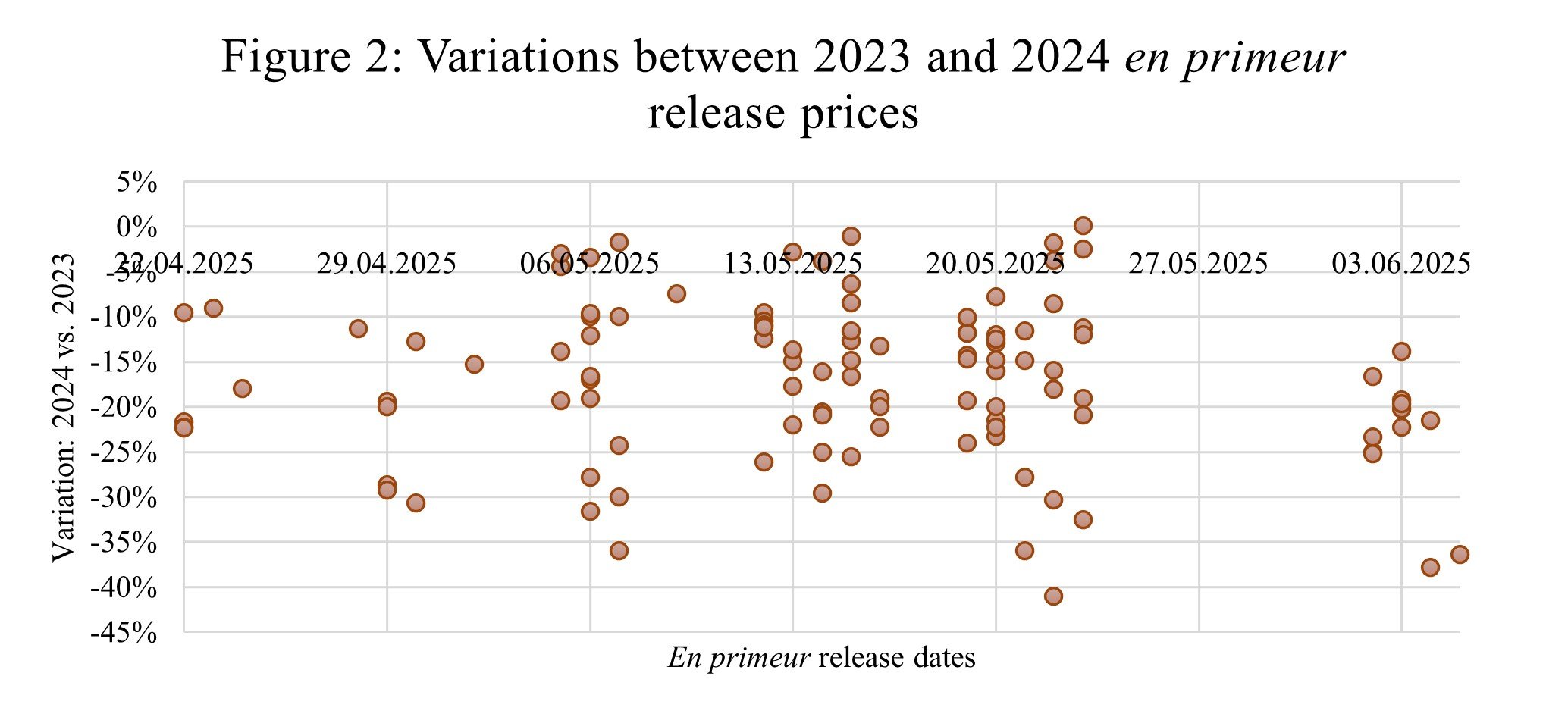

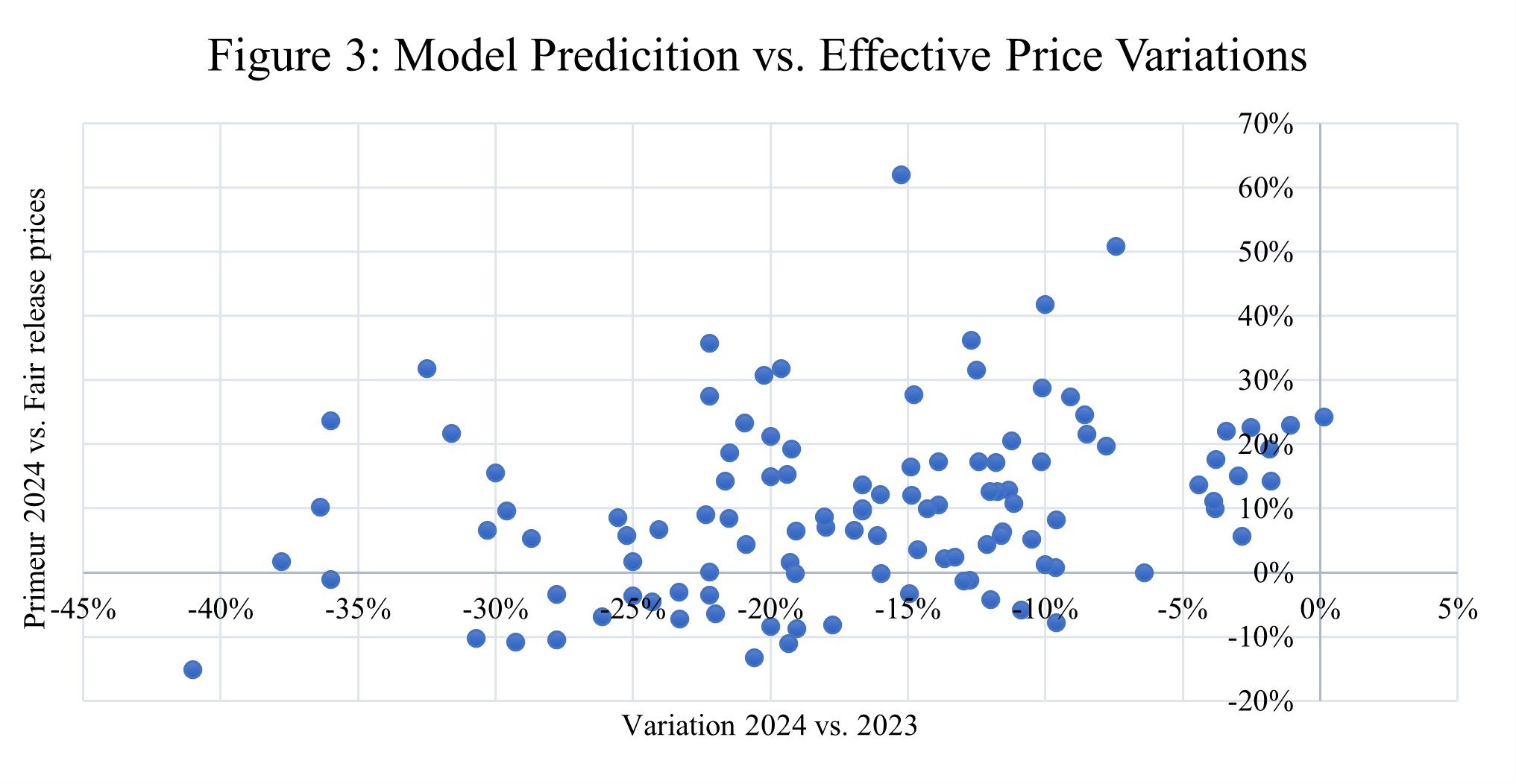

At first glance, the 2024 en primeur campaign resembles a clearance sale. But is that truly the case? Figure 3 compares the change in release prices between the 2023 and 2024 vintages with the deviation from the fair price estimated by the model. Wines in the upper quadrants were released at prices higher than those considered fair by the model; those in the lower quadrants were released below the model’s estimate. Two key insights emerge, shedding light on the strategies adopted by certain châteaux. First, a majority of wines were released at prices exceeding the fair value suggested by the model, sometimes by as much as 40% to 60%. Only about a quarter of the wines were priced in line with, or below, the model’s fair value estimate. Second, there is a clear correlation between the magnitude of price reductions from 2023 to 2024 and how close the release price is to the model’s prediction. In other words, the châteaux that made the largest price cuts are often those whose 2024 prices now align more closely with the model’s fair values.

— Source: EHL

The wines analyzed are listed in Exhibit 1 and classified into four categories: category A contains wines with a release price at least 5% lower than the fair price as estimated by the model; category B contains wines with a release price between -5% and +5% of the price estimated by the model; the last two categories contain wines with a release price 5% to 20% (C) or more (D) higher than the price estimated by the model.

Exhibit 1: Pricing by château

Category A: Wines with a release price at least 5% below the model’s estimated price.

Angélus, Batailley, Carruades de Lafite, Cheval Blanc, Clos Fourtet, Durfort-Vivens, Haut-Brion, Kirwan, La Lagune, Lafite Rothschild, Le Petit Mouton de Mouton Rothschild, Les Carmes Haut-Brion, Mouton Rothschild, Pavie.

Category B: Release price between -5% and +5% of the model’s estimated price.

Alter Ego de Palmer, Ausone, Beau-Séjour Bécot, Brane-Cantenac, Clerc Milon, Clinet, d’Armailhac, Echo de Lynch-Bages, Faugères, Figeac, Haut-Bages Libéral, La Chapelle de La Mission Haut-Brion, La Mondotte, Larcis Ducasse, Lascombes, Le Marquis de Calon Ségur, Le Petit Lion du Marquis de Las Cases, L’Evangile, Lynch-Moussas, Château Margaux, Pavie-Macquin, Pavillon Rouge du Margaux, Prieuré Lichine, Talbot.

Category C: Release price 5% to 20% higher than the model’s estimated price.

Beychevelle, Blason d’Issan, Branaire-Ducru, Calon Ségur, Canon-La-Gaffelière, Cantemerle, Cantenac Brown, Chasse-Spleen, Clos du Marquis, Corbin, Cos d’Estournel, d’Issan, Domaine de Chevalier, Ducru Beaucaillou, Duhart-Milon, Fombrauge, Gazin, Giscours, Gloria, Grand-Puy Ducasse, Grand-Puy-Lacoste, Gruaud Larose, La Croix Ducru-Beaucaillou, La Dame de Montrose, La Fleur-Pétrus, La Tour Carnet, Lagrange, Langoa Barton, Laroque, Le Dragon de Quintus, Léoville Barton, Léoville Las Cases, Léoville Poyferré, Lilian-Ladouys, Lynch-Bages, Malescot Saint-Exupéry, Montrose, Pagodes de Cos, Phélan Ségur, Pichon Comtesse Réserve, Pichon Longueville Comtesse de Lalande, Potensac, Rauzan-Ségla, Saint-Pierre, Sociando-Mallet, Soutard, Trotanoy, Trotte Vieille, Valandraud, Vieux Château Certan.

Category D: Release price at least 20% higher than the model’s estimated price.

Bélair-Monange, Canon, Carbonnieux, Beausejour (Duffau), Chauvin, Cos Labory, Dauzac, du Tertre, Haut-Bailly, Haut-Batailley, La Clotte, La Conseillante, La Mission Haut-Brion, Lafleur, Latour Martillac, Le Clarence de Haut-Brion, Malartic Lagravière, Ormes de Pez, Palmer, Pape Clément, Peby Faugères, Pichon Baron, Pontet-Canet, Quintus, Rouget, Smith Haut Lafitte, Troplong Mondot.

Most of the 1st growths are in category A. They reduced their prices to align with the secondary market. Categories A and B also include a number of châteaux that have, for several years now, consistently adopted pricing strategies in line with secondary market conditions. Examples include Brane-Cantenac, Clinet, Pavie Macquin and Talbot. Excluding premier crus classés, the most attractively priced wines relative to the model are Carmes Haut-Brion and La Lagune. Various reports suggest that Carmes Haut-Brion is one of the few wines to enjoy a certain degree of success this year.

Super seconds (i.e., wines that are at the top in terms of quality and reputation but not officially classified 1st growths) are in a complicated situation. Most of them fall into categories C and D. They are clearly trying to avoid diluting their brand by cutting prices too sharply. Some are also suffering the consequences of having set prices far too high for the 2022 vintage, and not reducing them sufficiently for 2023, leaving them with a correction that is difficult to make in a single campaign. Others, known for their historically reasonable pricing, may feel they didn’t overprice in the past and therefore see no reason to drop significantly. The issue is that the secondary market for these wines has become particularly unfavorable over the past two years. So, even if their previous en primeur prices were in line with the secondary market, a more significant price cut for 2024 would have been necessary to maintain that alignment.

Among the wines priced highest relative to the model, we find a mix of châteaux with more modest reputations and limited flexibility to adjust prices, estates that are (re)positioning themselves and seeking to support their brand image through elevated pricing, and wines with very limited production that are likely less sensitive to demand fluctuations. A good example is Lafleur: its release price remains virtually unchanged from 2023, yet it is still offered in limited quantities by several merchants.

Bordeaux En Primeur: A Market at a Crossroads

Bordeaux and its en primeur wines no longer ignite the same passion. Among the various reasons behind this waning enthusiasm, one stands out in particular: pricing. Too often, release prices are disconnected from the realities of the secondary market. Nearly all recent vintages have been launched at inflated levels. Even 2019, once praised for its strong value proposition, now sees several wines trading at or even below their 2020 release prices.

For the 2024 vintage, châteaux were faced with three strategic options:

Release at the fair price, in line with the secondary market and the model’s estimates. This is a prudent approach: while it may not generate immediate commercial success, it helps preserve the estate’s reputation and supports long-term brand equity.

Release above the fair price. This is a riskier bet: it can lead to weak sales and, over time, erode the château’s image.

Release below the fair price. This can foster goodwill among buyers and ensure strong distribution of the vintage. However, it is only sustainable if the price remains consistent with the estate’s long-term positioning and perceived value.

For consumers, the rule is straightforward: there is no rational (or even emotional) justification for purchasing an en primeur wine priced above its estimated fair value. The secondary market offers plenty of more compelling alternatives. Wines priced in line with model predictions aren’t necessarily bad buys, but they don’t warrant immediate action either. Conversely, wines offered below their estimated value may represent genuine opportunities. 2024 is a good vintage (we rarely see truly poor vintages anymore). The wine market, being highly cyclical and emotionally driven, is currently in a downturn. In this context, a wine that appears relatively underpriced is an opportunity well worth seizing.

A point not addressed in this article, but which further reinforces the prevailing uncertainty, is the geopolitical context. In particular, trade tensions and US tariffs are weighing on demand and calling for heightened vigilance.

It remains surprising that, years after Ashenfelter’s (2008) article, the wine market is still largely inefficient, with prices often misaligned with market fundamentals. Far from correcting itself, this inefficiency has worsened, to the point of threatening the sustainability of the Bordeaux system. This inertia weakens the entire value chain – producers, négociants, and consumers alike. While this article does not aim to analyze the root causes, a collective effort is urgently needed. A strategic wake-up call is now indispensable.

References:

Ashenfelter, O. (2008). Predicting the quality and prices of Bordeaux wine. The Economic Journal, 118(529), F174-F184.

Cardebat, J. M., & Paroissien, E. (2015). Standardizing expert wine scores: An application for Bordeaux en primeur. Journal of Wine Economics, 10(3), 329-348.

Masset, P., Weiskopf, J. P., & Cardebat, J. M. (2023). Efficient pricing of Bordeaux en primeur wines. Journal of Wine Economics, 18(1), 39-65.